Debunking Popular Myths About Mining Pools

Mining pools are often surrounded by myths and misunderstandings that can mislead both newcomers and experienced members of the cryptocurrency community. These myths not only distort the understanding of how mining pools actually work but can also influence decisions regarding investment and participation in mining. Let’s debunk some of the most common myths.

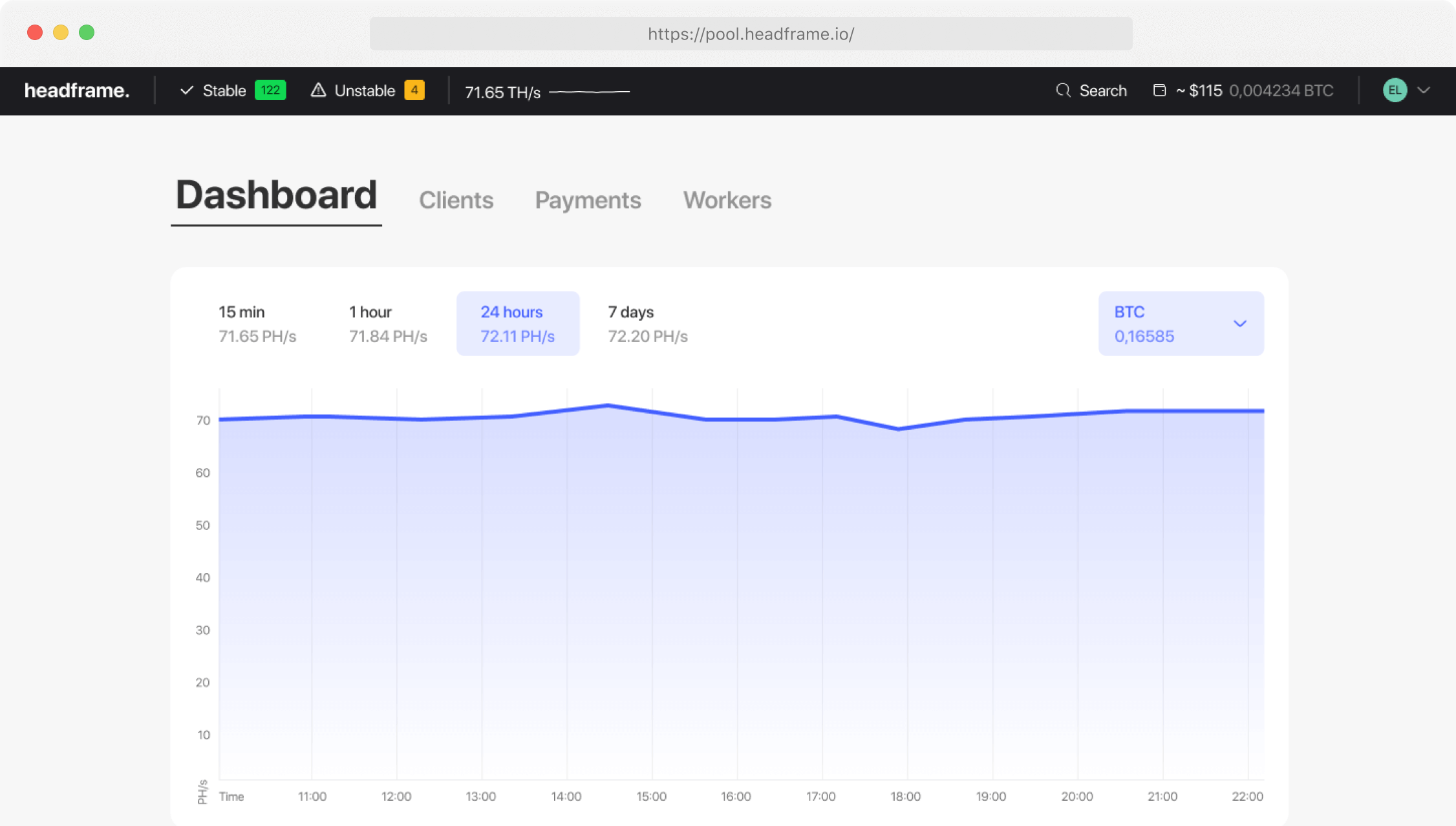

Earn more money with Headframe

Получите лучшую доходность в майнинге. Самая низкая на рынке комиссия 0.9%, обход блокировок и ежедневные бесплатные выплаты.

Myth 1: Mining pools guarantee higher profits compared to solo mining.

While joining a mining pool can indeed increase the regularity of payouts by pooling computational power and increasing the chances of successfully mining blocks, it does not always lead to higher profits. The fees charged by mining pools and the competition within the pool can reduce the actual profit of each participant.

Myth 2: Mining pools control the blockchain and can manipulate transactions.

In reality, despite large mining pools owning a significant share of the hashrate, the blockchain protocol requires transaction confirmations from various network nodes, making it extremely difficult for one organization to manipulate or control the network. The blockchain is designed to prevent such possibilities through decentralization and consensus.

Myth 3: Mining pools contribute to increased centralization in the blockchain.

Although the concentration of hashrate in the hands of a few large pools can potentially pose such a threat, many mining pools strive to maintain network decentralization by actively supporting and promoting numerous smaller pools and offering innovative solutions to reduce their dominance.

Myth 4: Mining pools are becoming obsolete due to the rise of alternative consensus algorithms like Proof of Stake.

In practice, mining pools continue to adapt, developing technologies and strategies to maintain their relevance and efficiency. They explore and integrate new methods, including hybrid approaches to mining and staking, to meet the needs of various blockchains and provide income opportunities for their participants.

Myth 5: Mining pools are unfair and do not provide equal opportunities for all participants.

In reality, many mining pools strive to ensure transparency in their operations and fair distribution of rewards. This is achieved through well-defined rules and terms of participation, guaranteeing that each miner receives a share of the revenue proportional to their contribution to the pool’s computational power.

Myth 6: Mining pools are an easy and simple way to earn money with cryptocurrencies.

In fact, successful participation in a mining pool requires an understanding of both the technical aspects of mining and the current market dynamics of cryptocurrencies. Participants must be prepared for potential changes in mining profitability due to fluctuations in cryptocurrency prices, increased mining difficulty, or changes in legislation.

Myth 7: Mining pools do not contribute to the development of blockchain technologies.

On the contrary, many mining pools actively participate in developing new technological solutions, invest in blockchain security, and support network upgrades, contributing to the improvement and optimization of blockchain infrastructures.

Myth 8: All mining pools are the same.

In reality, differences between mining pools can be significant, including varying fee structures, reward distribution methods, levels of user support, and technical capabilities. Therefore, it is important to conduct thorough analysis and choose a mining pool that best meets the individual needs and expectations of the miner.

Debunking these myths not only helps better understand the real state of affairs in the world of mining pools but also promotes more informed and effective participation in cryptocurrency mining.